October 2017 | Signature Research

The Next Generation of Health IT Spend: Where Should Health Systems Invest?

Hospital leaders must determine which investment strategy aligns with their business strategy. Our research identifies three IT investment profiles for the future.

Get the full reportIntroduction

The growth rate in hospital IT spend has outpaced growth rates in overall healthcare costs by as much as five times between 2007 and 2015, according to analysis conducted by West Monroe Partners. Much of the IT spend during that time was dedicated to massive investments in electronic health record (EHR) implementations.

Hospitals now face a post-EHR era where, absent federal incentives and directives, executives are left to decide on their own which technology investments to undertake, and whether to slow their spend. Given current market forces, from consumerism to reimbursement pressures, our point of view is that IT spend relief is not in sight unless hospitals plan to remain a traditional utility player. According to our research, hospitals of the future will fall into one of five investment profiles:

1. Traditional utility

2. Home-grown experimenters

3. Leveraged experimenters

4. Home-grown innovators

5. Leveraged innovators

To move forward, hospital leaders must first determine which of these five investment profiles aligns with their business strategy. This paper outlines a set of navigating principles to help executive teams identify the appropriate investment profile for their organization.

Chapter 1: The rise and fall of IT spend: 2009 to 2015

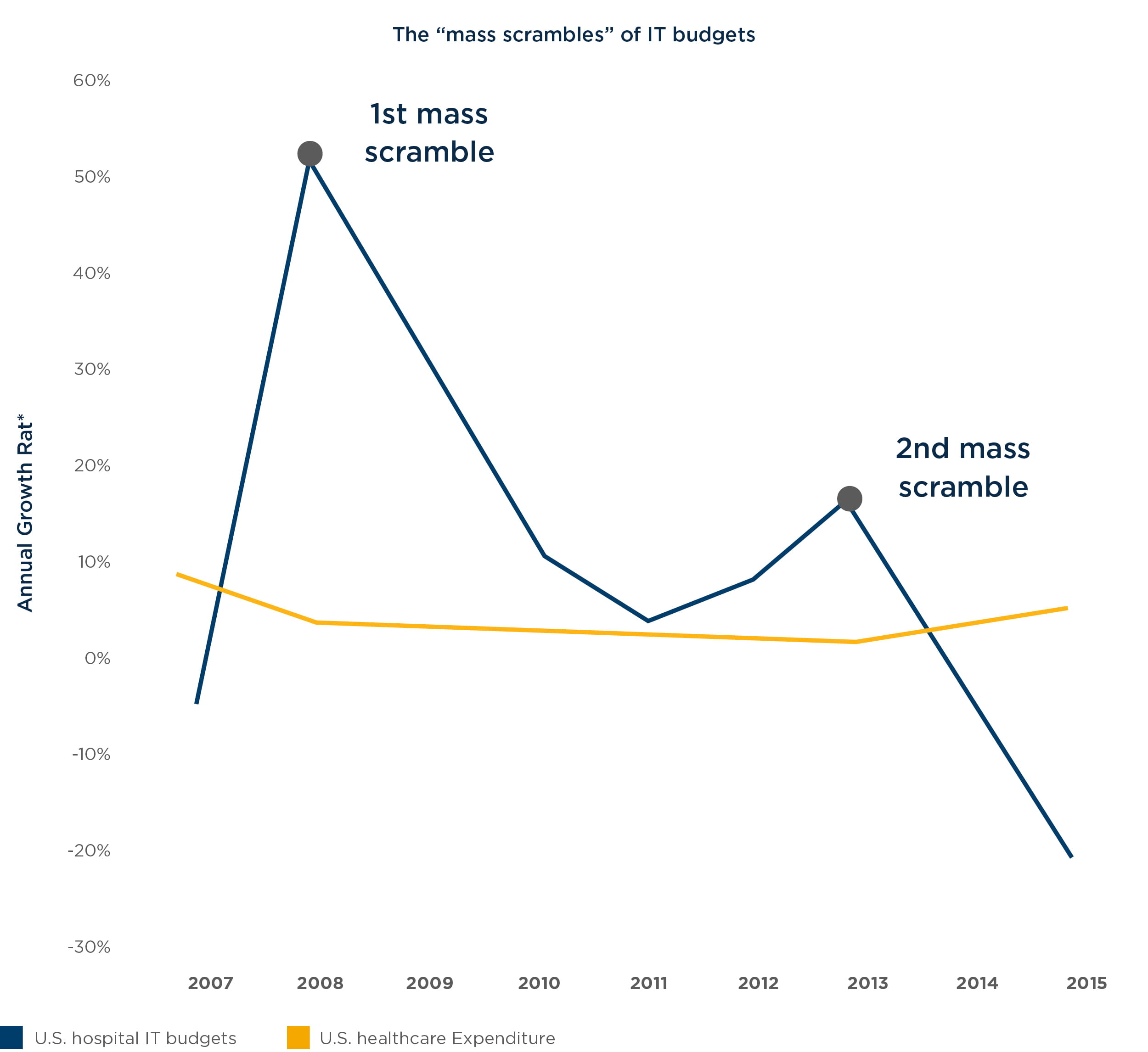

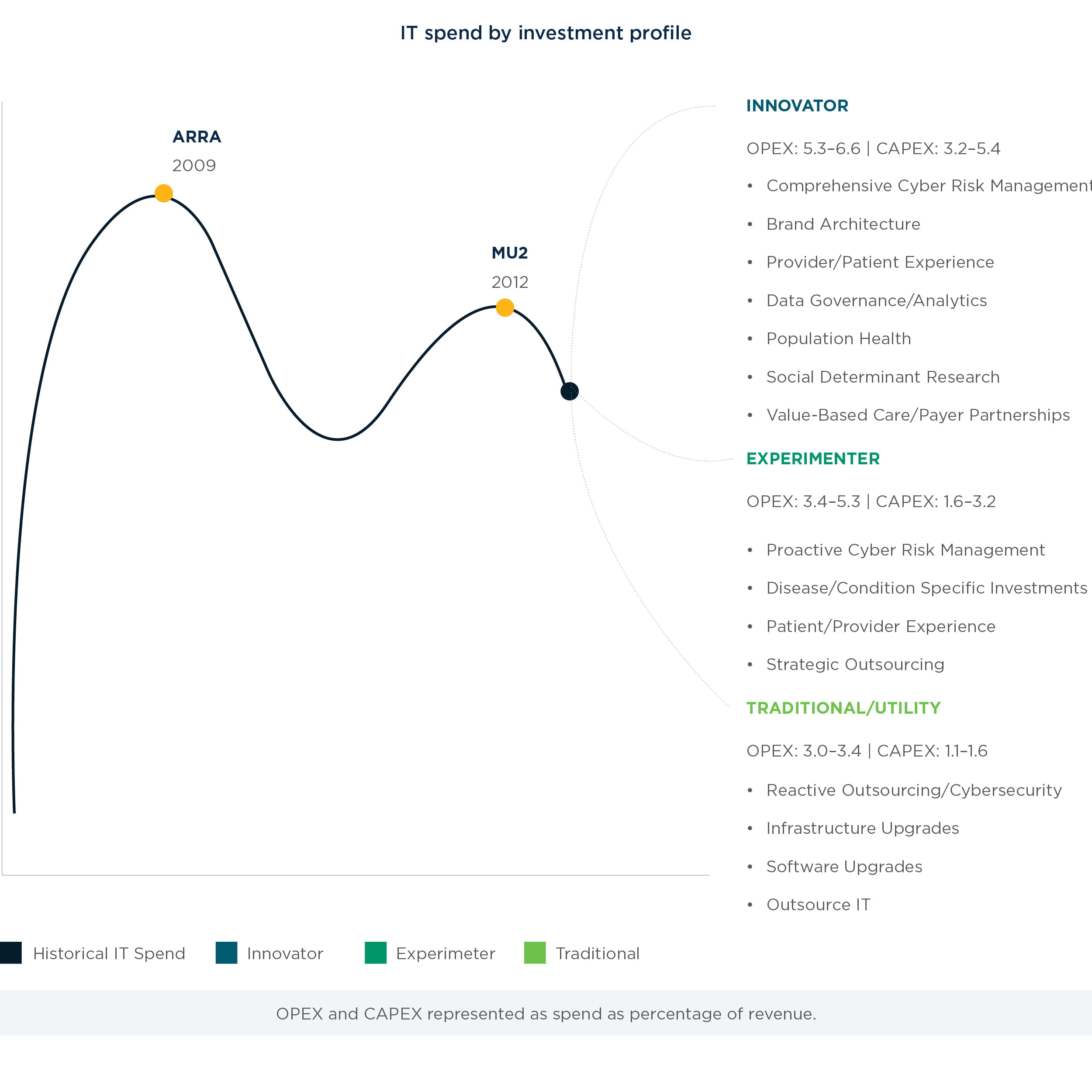

Fueled by legislative and regulatory changes, hospital IT budgets – and specifically EHR investments – spiked over the last decade, outpacing overall healthcare expenditure growth. As most health systems faced new requirements, they invested $15,000 to $75,000 per provider, but also organizational capital to focus on meeting these requirements – in a way, conducting “mass scrambles.” Looking at the growth rate of IT spend and overall growth rate of investments (Figure 1), two mass scrambles stand out. The first was driven by the American Reinvestment and Recovery Act (ARRA) stimulus package that provided approximately $27 billion in reimbursements for health IT. In the two years prior, providers were already investing heavily in EHRs as they anticipated the government’s involvement – ARRA sealed the deal in February 2009. Near the end of the ARRA stimulus package timeframe, late adopters fueled another boost in spend to complete implementation of EHR systems in time to receive reimbursements and meet Meaningful Use requirements by the end of 2012.

This phase of intense IT spending represented a long-overdue “catch-up” to convert manual processes (e.g., charting, scheduling) to the modern world of connected, electronic systems, similar to conversions seen in the banking sector in the late 1990s.

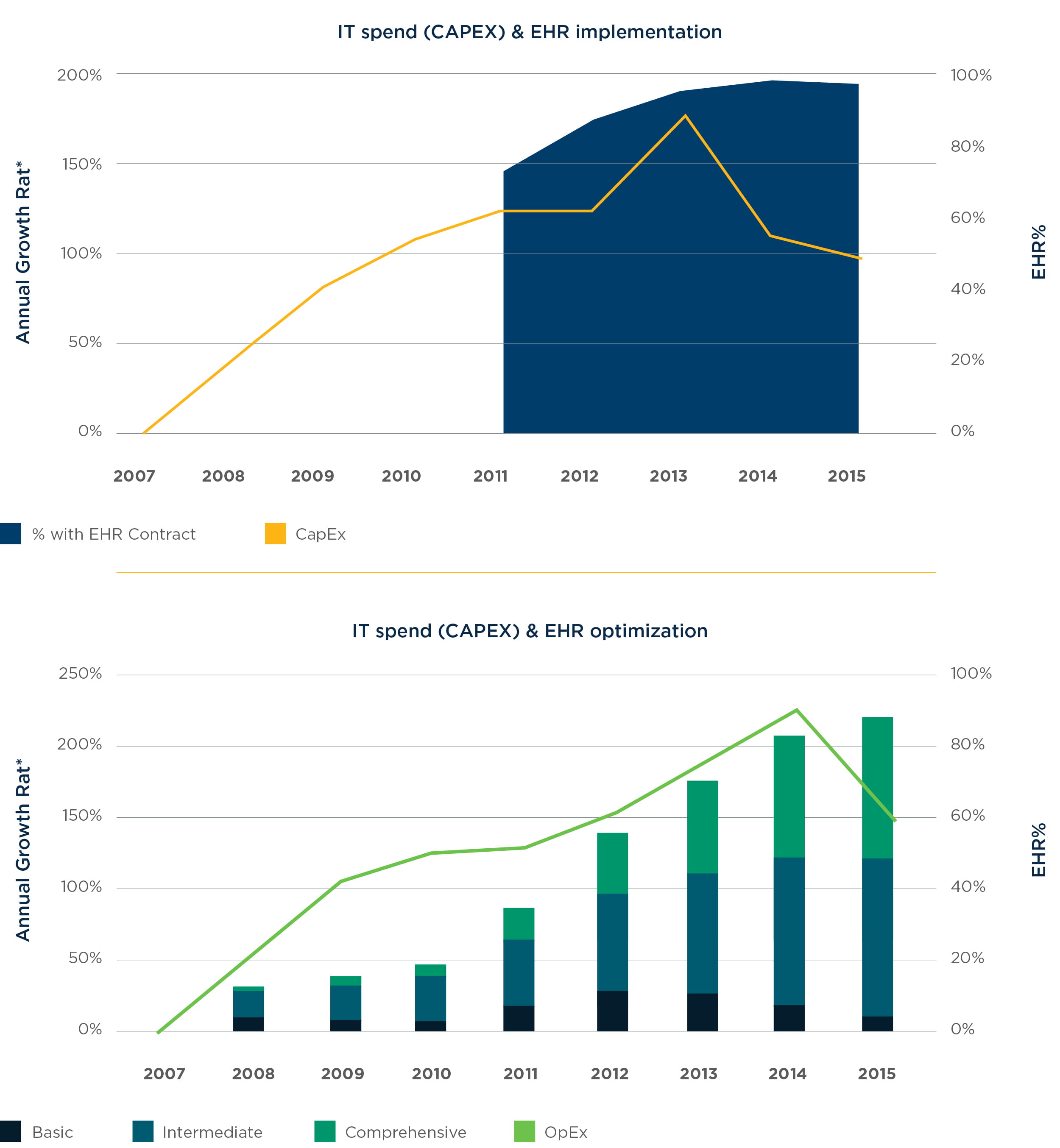

In 2013, IT capital expenditures sharply decreased while operational expenditures continued to increase (Figure 2). This was due to many EHR systems providing only the basic framework and digitization of patient records – the connectivity, usability and other functionalities that make these electronic systems worthwhile were all pushed off into a phase now called “EHR optimization.” By 2014, 96% of providers had implemented EHRs, essentially reaching saturation and decreasing the rate of aggregate IT expenditure growth (Figure 3).

At this point, health system leaders began to question whether relief from IT spend was in sight. With billions spent on EHRs, and now billions more being spent on implementation, budgets have remained at peak levels. And health system executives are asking, “What’s next?”.

Chapter 2: A complex industry demands complex technology investment

As health system leaders enter a new phase of IT spending, they have the following options:

- Cut IT spending

- Continue to invest in new IT solutions

- Address accumulated technology debt from other neglected systems

Which route should a health system choose? To answer that question, we must first consider the current market forces that are evolving the technological landscape.

1. Reimbursement Pressures

As reimbursement rates are increasingly tied to health outcomes and not services provided, technology investments will be a crucial step in transitioning away from the fee-for-service model. Hospitals are facing increased pressure to comply with quality and safety standards and at the same time improve patient care, satisfaction, and experience to meet requirements for higher reimbursement rates. While the industry is shifting, albeit slowly, hospitals are beginning to experiment with value-based care delivery models including bundled payments and shared savings – both of which require new capabilities anchored by technology.

2.Consumerism

Healthcare is a unique industry, where the consumer has historically had little to no involvement in payment for services. With primary purchasers of healthcare services being third- party payers, the consumer is often left out of buying decisions and given little to no incentive (or knowledge) to question the cost or quality of care they receive. Yet, this relationship between healthcare buyers and consumers is being rapidly dismantled. Demands for greater transparency around the cost and quality of care have led to consumer-driven health plan design with greater shares of cost falling to consumers themselves.

Digital health has also ushered in the opportunity to give consumers more control in managing their personal health. With expanded choice, patients are beginning to shop around not only for health plans, but also providers, including standalone clinics and telemedicine. Consumers appear to be loyal to their doctors, but not their health system, placing higher value on convenience and overall experience than brand loyalty. In fact, the Centers for Medicare and Medicaid (CMS) has tied 25% of reimbursement to patient experience. As consumers expect greater convenience, they demand greater automation and ease in handling logistics via technology.

3. Regulatory Changes

An increased number of regulations are having a direct impact on health systems and patient care, such as the Affordable Care Act (ACA), Health Information Exchanges (HIE), and Meaningful Use. While the benefit or harm of any of these regulations are debatable, what is clear is that health systems have more rules to follow, and technology is often a part of keeping up with these rules.

4. Population Shift

The population is aging: By 2050, those 65 or older will represent 20.2% of the U.S. population, compared to 8.1% in 1950. And the degree of cultural and linguistic diversity is increasing rapidly. A more diverse patient population means increasing complexities in managing patient care that extend beyond a clinic and include explanation of health benefits, patient advocacy, multilingual resources, home-based care, and even transporting patients to and from clinical sites. With a more complex and diverse patient pool, technology can be leveraged to accomplish more with fewer providers.

5. Security

With increased technology adoption, hospitals face increased threats in cybersecurity. The Federal Bureau of Investigation had warned the healthcare industry to prepare for cyber threats. According to the Ponomon 2016 Cost of Data Breach Report, done in conjunction with IBM Security, the average cost per stolen record was $355.5 Healthcare is a high-risk industry when it comes to the cost of stolen records since the information contained is more valuable to the hackers for identity theft.

These five forces at play indicate that there are several growing needs for IT within health systems. Relief from IT investments is likely not in sight, and in fact, a second wave of IT investments is on its way. But how should health systems react to this next wave of spend? Should they seek to minimize it? Ride the wave like the first two mass scrambles? Is there any way to be more deliberate with investments to get ahead of the curve? Given the complexity of the healthcare environment, technology adoption can be equally complex. While most health systems have been in reactive technology mode, they seek a more proactive approach.

How does your organization approach IT?

Before an organization is able to determine which investment profile is the best fit, they first need to decide what type of technology approach they should adopt.

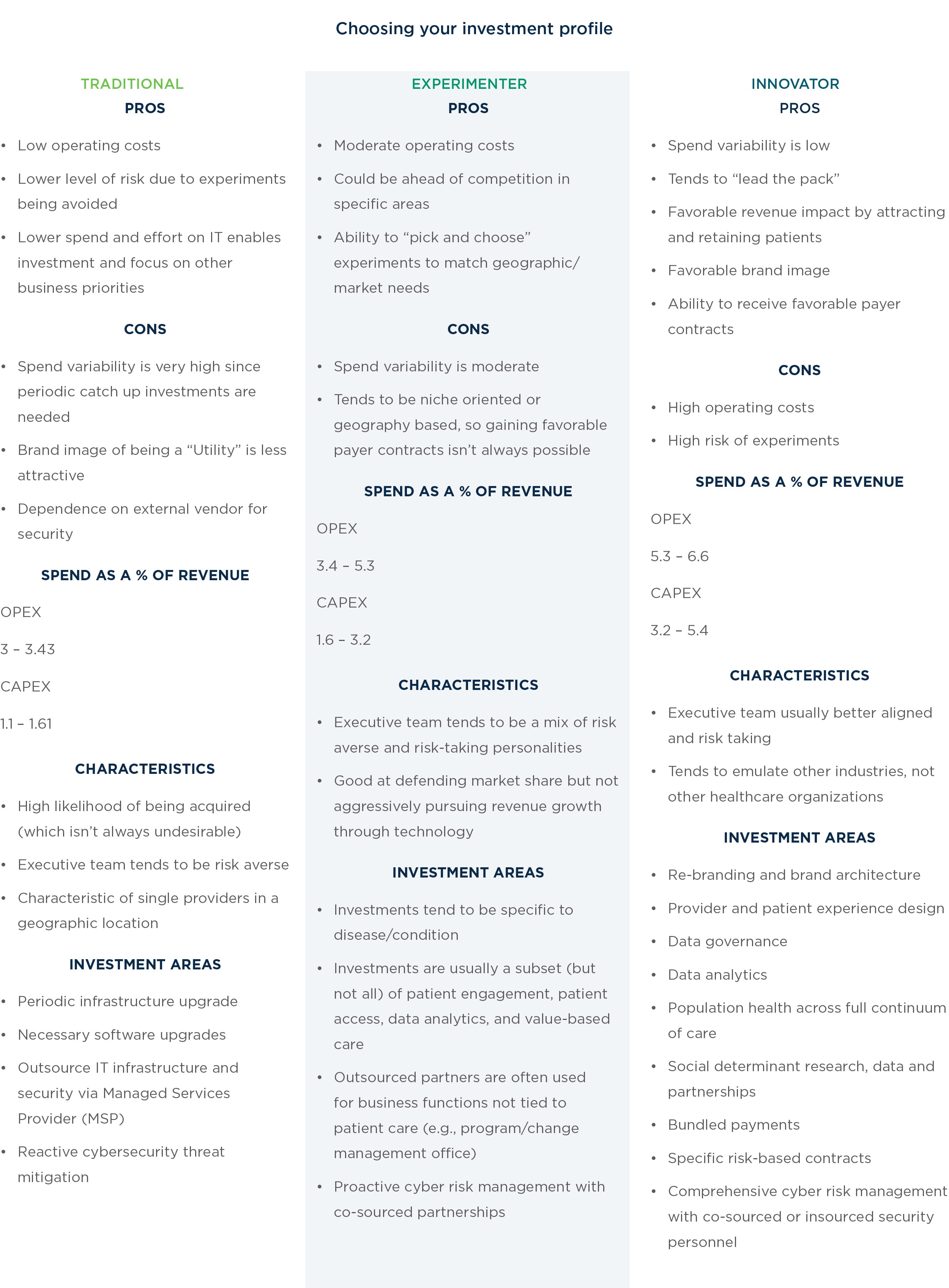

Traditional: Traditional players use IT as a utility and cost center. The organization spends resources on other business areas (primarily facilities, but also quality, safety, patient care, etc.), while IT plays a support function.

Experimenters: Experimenters use IT as a cost center for most functions, but for select functions, technology partners with the business to either improve operational efficiency and reduce cost, and positively affect revenue. Cost reduction might be in areas such as health information management, billing and revenue cycle, clinical documentation, and others. Revenue enhancement could be around patient experience or referral leakage.

Innovators: Innovators are consumer-centric, seeking to deliver a superior consumer experience via a superior provider experience, and one that is constantly innovating and leveraging technology. It is inspired by other industries’ use of technology while learning from the best of its peers in healthcare.

Technology is both a driver of revenue as well as an optimization of costs. An innovator plans to repurpose existing revenue streams (such as fee- for-service revenue or emergency department revenue) as they evolve to match the changing needs of the market toward value-based care. An innovator has a continuous process of churning small experiments and declaring victory or loss on such experiments, essentially failing fast and succeeding fast.

Deciding what to insource and what to outsource

Different investment strategies call for different ways of approaching technology talent. Do you employ every technology resource? Do you outsource certain skills or functions? These questions are answered within each investment profile.

There are many different types of technologists. Some are “operators” who are best at running the IT operations in a highly cost-effective manner.

Others tend to be “innovators” who find intrigue in developing new and innovative solutions. Once the mix of team members is determined, the mix of insourced versus outsourced services should be decided. Lastly, heath system leadership can define the technology CapEx and OpEx expenditures.

When deciding on these three elements, each blend implies a variability in the cash outflow.

Traditional: The Traditional player tends to insource as much of the IT personnel as possible to keep costs low in supporting basic operations. Some roles may be outsourced around certain areas like security services. For example, instead of hiring a Chief Security Officer, a traditional player may use a virtual Chief Information Security Officer (CISO).

The personnel hired are meant to simply run the operations in a steady manner and are not required to be innovative. When it comes to OpEx spend, it is lowest among these systems while CapEx will likely be higher due to high number of insourced functions. The spend variability tends to be higher for a traditional player since there will be assets that have a multi-year lifecycle needing upgrades every few years, causing spend to spike some years while being lower other years.

Experimenter: An Experimenter is a Traditional player who also seeks to support some targeted areas of investment. There are three types of experimenters:

Home-grown: This experimenter wishes to keep innovation and talent in-house. Typically, Home-Grown Experimenters tend to be academic medical centers or health systems that reside in metropolitan areas where innovative technology talent is abundant. The tendency is to keep as many of the innovative/transformational types of personnel in house. The OpEx spend is larger than that of Traditional Players due to higher-skilled insourced personnel and even some outsourcing. CapEx tends to be similar to Traditional players, perhaps slightly higher. Spend variability also tends to be volatile like Traditional players.

Leveraged: A Leveraged Experimenter wishes to keep a smaller internal staff to keep costs low and outsource via partners to conduct innovative/transformative technology work. A health system would tend toward this composition when innovative/transformational talent is difficult to find and retain. Such health systems must form strong partnerships in the vendor ecosystem to find leveraged innovators. CapEx/OpEx composition tends to be similar to Home-Grown and spend variability is also similar with strong strategy and budgeting processes in place, so that year-over-year “experiment” budgets with partners are anticipated.

Innovator: An Innovator is an experimenter who considers innovation a part of doing business and experimentation becomes a key part of both long- term strategy and day-to-day operations. Similar to the Experimenter, Innovators can be home- grown or leveraged and face similar compositional qualities with a few differentiators: The level of CapEx/OpEx investments are higher than that of an Experimenter; the innovation pipeline is much larger and diversified – across patient engagement, analytics, technology driven patient care, revenue models etc. – as a result variability is lower than that of an Experimenter; and budgeting and governance is a much more mature process.

Navigating principles for the road ahead

Deciding which technology profile, and corresponding investment strategy, is right for you cannot be easily accomplished. No two health systems are the same and navigating the road ahead is not formulaic. In addition to considering the characteristics of each investment profile, the following principles can help reveal the right technology strategy for your organization.

-

Culture is your most intangible asset. You simply can’t transform yourself to be the hospital of the future without transforming culture. If you don’t have a grounded strategy and plan to transform your culture, transforming your hospital is merely wishful thinking. Having buy-in and alignment of the executive team is often easier said than done. Nevertheless, without alignment, know that all brilliant ideas are ultimately just that, a brilliant idea.

-

Ensure your perceived market position matches your actual capabilities. It is critical to be honest with who you truly are as an IT organization. Oftentimes health system IT organizations desire to be more than their capabilities and underplay their capabilities or appetite for experimentation when working with the rest of the business. At times, the given geography may allow for a health system to appear more innovative when they are truly an experimenter at best. In such situations, it’s acceptable to utilize such market forces to their advantage if and only if the system is able to deliver what it promised.

-

Cut your cost intelligently in areas not directly tied to patient care. Cutting costs has become an overused temporary solution for many health systems. Though it makes sense to do so to provide temporary relief, cutting costs in critical areas such as security or areas that will allow for greater patient engagement is only going to hurt the system in the long run. Additionally, health systems do not have the culture of outsourcing functions like data centers, virtual CISO services, and program management. Health systems should strategically outsource IT functions according to the needs of their investment strategy.

-

Start with small data and earn your way into big data. Most big data initiatives fail due to massive transformational changes all occurring at once. There is plenty of low-hanging fruit that health systems can execute such as readmissions reduction and chronic care management. Proving positive ROI or positive impact to the mission of the hospital is more likely to earn your organization the ability to invest in larger data analytics initiatives.

-

Know which Key Performance Indicators (KPI) you own as IT and ones you own in partnership with the business. As IT organizations become more innovative, they should start to co-own some KPIs and become a true partner and not only just a technology provider. For example, a utility IT department may have KPIs such as total spend, total spend as percentage of budget etc. But a truly innovative IT department may co-own metrics with the business, such as percent of appointments made without manual intervention.

-

Reinvent yourself. It’s a key step to reinventing your hospital. Health system IT departments need to rebrand themselves internally as the hospital begins to rebrand itself to the external market. It’s virtually impossible to keep up with the changing demands of a rebranded hospital without having a solid rebrand internally supported by key stakeholders.

Conclusion

Learn how to create a strategic road map

Calculating strategic investments in technology is a key question for health systems today, and current market trends show no sign of diminishing importance of these investments in years to come. Such a strategic process is never linear. However, the first step within the process — picking an investment profile and thereby rightsizing what you will spend on IT — is something that can be done via a prescriptive, linear process outlined in this paper.

Becoming an organization that is proactive about IT is difficult in an industry where revenue, investments, and policies are highly regulated. But it is possible — and imperative — for health systems to innovate at the speed of market, so they can serve the patients of tomorrow while not losing focus on the patients of today.