November 2015 | Signature Research

Keeping the Lights On: Addressing the challenge of Distributed Energy Resource Growth

The rise of distributed energy resources (DERs) is an exciting and interesting opportunity for customers, and a challenge and opportunity for the utilities and the organizations that regulate them

Get the full reportThe rise of distributed energy resources (DERs) is an exciting and interesting opportunity for customers, and a challenge and opportunity for the utilities and the organizations that regulate them. DERs is a category of solutions that is inclusive of distributed generation sources like combined heat power (CHP), solar, and wind, as well as energy storage such as batteries. In this white paper, West Monroe takes a comprehensive look at how consumers, utilities and regulators are approaching – or resisting – this energy evolution. This research examines the present and future state of DERs through multiple lenses: customer adoption and awareness; utilities’ adoption challenges and opportunities, and support and planning initiatives; and regulatory commissions’ actions, obstacles and perceptions.

We found that while the presence of DERs among residential, commercial and industrial sites is still limited, customer interest is increasing and adoption is on the brink of booming in many states across the U.S. And though utilities and regulators alike acknowledge this potential shift, in many states they have yet to settle on clear and collaborative ways to prepare for it. Factors from technology availability and cost, to public policy drivers, to pivoting business models, are contributing to the obstacles slowing DER penetration across the U.S. These issues continue to impede the industry’s ability to smoothly accommodate new energy technologies and gain acceptance. By illuminating the gaps between customer needs, utility plans and regulators’ perceptions, it is evident that these audiences must form a more united front before meaningful change can truly occur in their state.

Introduction

The electric utility industry is accelerating toward a crossroads. Cost-averse and environmentally conscious customers are reducing their dependence on traditional utility generation and creating increased demand for distributed energy resources (DERs). If the market’s recent growth is any indication, DERs will become a more important part of the generation portfolio mix in the future.

Between the U.S. federal government’s enactment of the Investment Tax Credit (ITC) almost a decade ago and launch of the SunShot Initiative in 2011, the cost of solar energy installations has plummeted more than 73 percent. This trend is aided by the U.S. Department of Energy’s decision to double down on its support for renewable energy research and development and materials manufacturing. While technology costs continue to decline and efficiencies rise, rest-of-system costs are coming down as well, making photovoltaic (PV) solar more affordable. Federal support, along with utility and state-sponsored financial incentives for purchases and leasing of rooftop solar PV systems, has accelerated adoption of DERs by residential, commercial, and institutional customers.

In the last few years, the barriers to DER adoption have decreased significantly in many areas in the US. Solar generation is competitive with retail electricity prices in many parts of the country, and comparable to avoided transmission and distribution system upgrades in some utility jurisdictions. Cost reductions in DER implementation and interest in such systems apply across rooftop, utility- scale, and recently in community solar installations, providing opportunities for broad business and customer adoption. In 2014, a new solar project was installed every two-and-a-half minutes in the U.S.

As business and residential customers continue to seek more economical and sustainable energy solutions and utilities require cleaner energy power solutions to satisfy various regulatory requirements, distributed energy adoption does not appear to be slowing down anytime soon. General Electric predicts that annual distributed energy capacity additions will grow from 142 gigawatts (GW) worldwide in 2012 to 200 GW in 2020, an annual growth rate of more than four percent. Though this shift carries benefits for customers and the environment, it is forcing the utility industry and regulators to rethink the traditional utility business model and the sanctity of the utility franchise. As electricity generation becomes more decentralized and located closer to load, utilities are beginning to identify ways to maintain revenue and provide greater value to customers through alternative rate design, new utility business solutions, and creation of unregulated business enterprises.

Chapter 1: The impact of DERs

Distributed energy resources present a new layer of complexity to utilities’ operations, while at the same time promising to inject new life into the traditional business model. Eighty percent of utilities in our survey reporting have DERs on their systems, but executives and regulators do not share a common vision when it comes to how regulations currently (or should) impact DER support and ownership. Today, three percent of customers have renewable energy sources serving their homes, and 48 percent are considering doing so in the next two years. Only one percent of customers are enrolled in distributed generation programs through their local utility. The rapid rise of DERs on utility systems is also creating difficulties for utilities to enroll customers and manage the interconnection process. Many utilities and regulatory commissions are looking at electronic enrollment and interconnection software to improve customer engagement and satisfaction.

Seventy-nine percent of regulators feel that the current regulatory model allows and encourages utility ownership of DERs, compared to just over half (53%) of utility executives. This indicates a discrepancy between what utilities think they need in order to encourage and support DER ownership and implementation, and what regulators think utilities need. In certain markets, regulatory commissions think the regulatory paradigm supports DER deployment; however, they might lack the resources necessary to thoroughly investigate the regulatory changes needed to support utility investment and ownership.

Despite the number of utilities that report having DERs on their systems, only 37 percent offer DER-specific support services, systems or technologies. In the same way that smart grids have enabled utilities to transform how they distribute and bill for electricity, DERs open the door for utilities to capitalize on new business opportunities, including backup generation, load balancing capabilities, differentiated pricing regimes, and solar marketplace services such as vendor identification, financing, and maintenance. Many utilities, however feel the cost of creating these services outweighs the returns: 59 percent of executives say their utility plans to make no or minimal investments to support DERs on their systems unless mandated by regulators.

Early reactions to the rise of DERs

The majority of utility executives harbor mixed feelings about how DERs will affect their business. Regardless of how executives feel, an uptick in adoption is inevitable. Two-thirds (66%) of executives feel DERs are both a threat and opportunity for their businesses, three percent feel they are only a threat, and nearly a third (31%) feel they present an opportunity. Understandably, many executives seem confused or feel it is too early to claim that DERs will or will not wreak havoc on their operations. As discussed later in this report, executives’ actions reveal that most utilities treat DERs primarily as a threat.

Today, more than two-thirds (69%) of customers do not know if their utilities offer distributed generation enrollment, and 94 percent say their providers haven’t approached them about alternative energy options. This can lead to uncertainty and confusion about customer-sited DERs. As DER adoption grows, more customers will demand specific accommodations such as efficient distributed generation (DG) enrollment processes and management, and accessible DER diagnostics. Utilities that fail to provide a sufficient DER customer experience may suffer business and compliance consequences, and as a result, more oversight from regulators. Certain regulatory authorities (including the New York State Public Service Commission) are starting to require utilities to offer electronic DER enrollment to decrease customer effort and increase transparency around the DER interconnection process.

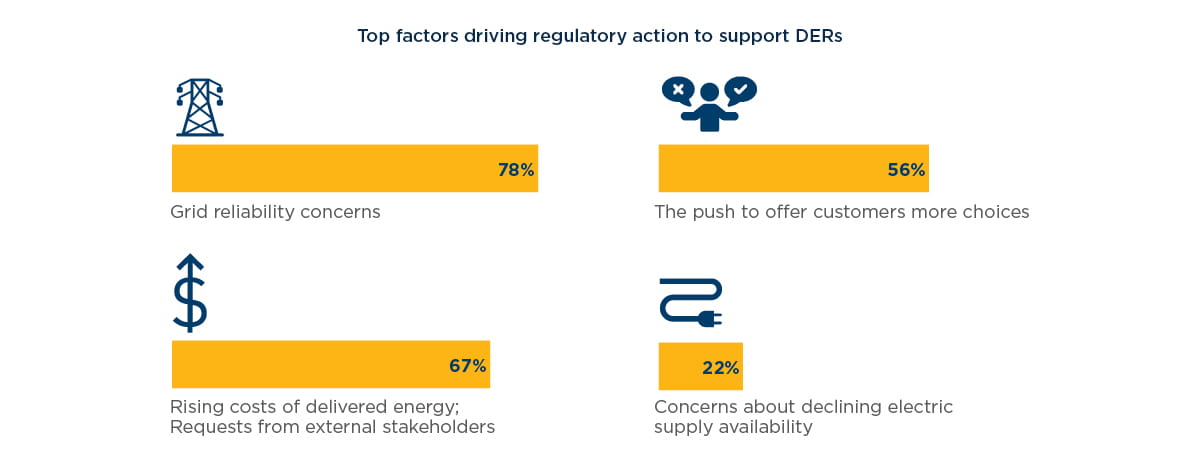

Regulators are already modifying their requirements and compliance paradigm to support DER integration. Regulators cited a handful of concerns driving the proposed changes:

Given the inherently polarizing nature of large-scale policy changes, utilities’ responses to regulatory modifications have been surprisingly positive. Two-thirds (67%) of regulators feel utilities have been responsive to regulatory changes, and half believe utilities are proactively adjusting their behaviors.

Breaking down DER implementations

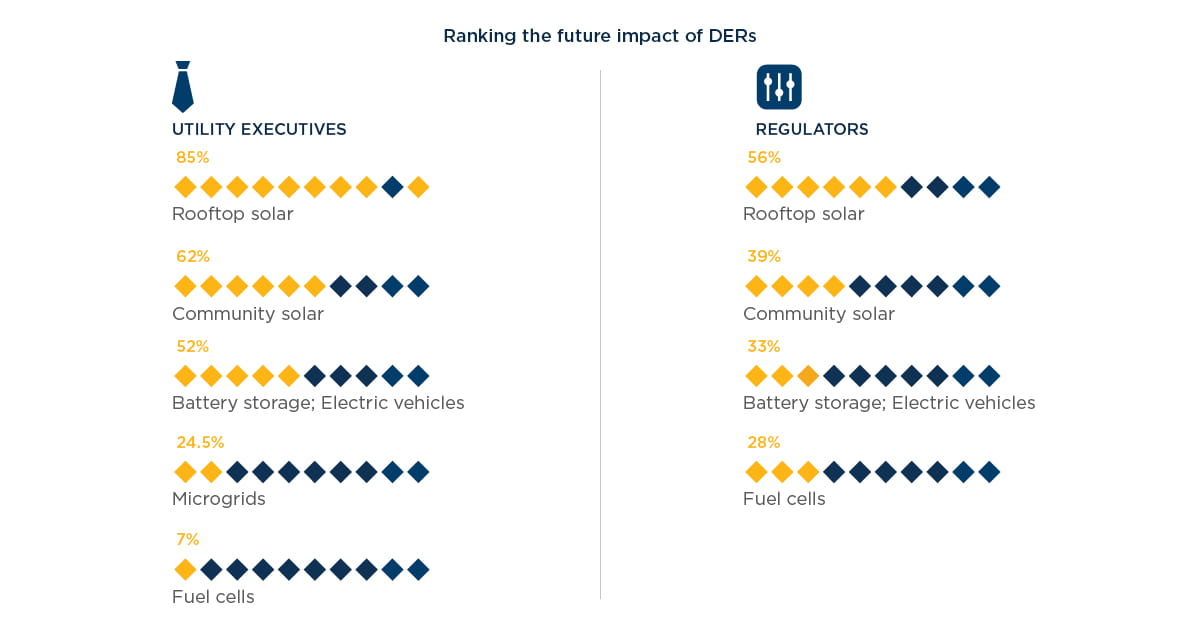

The selection of available distributed energy options is expanding. Utility executives and regulators agree that solar resources stand to have the greatest impact on utility operations and revenue streams, more than other emerging resources such as electric vehicles and microgrids.

There are several reasons for this, including solar’s proximity to load, ease of permitting and installation, and market awareness by non-utility and utility market participants relative to other renewable energy resources. Ninety percent of customers that have adopted renewable energy sources in their homes use solar systems, followed by wind turbines (7%) and hydropower systems (3%).

Chapter 2: Who’s really fueling DER adoption?

Commercial and industrial customers have long led the charge to adopt self-generation technologies, for a variety of economic reasons. In recent years, however, residential customers have begun to participate in the growth of DERs and enjoy the associated financial benefits.

Residential customers are the largest group adding DERs, cited by 82 percent of utility executives, followed closely by commercial and industrial customers (77%). Forty-four percent of executives claim utilities themselves were adding DERs to the grid, while 32 percent say the same of third- party power providers. Only 12 percent report aggregated communities as a contributor to DER adoption. That this audience is the smallest contributor to perceived levels of adoption – especially given utilities’ intention to reduce costs and provider greater customer choice – indicates potential improvements might be needed in order for the community aggregation model to provide greater value.

A combination of factors is impacting customers’ attraction to DERs, from the social elements (including a growing desire to protect the environment and be seen as responsible citizens), to the financial (such as taking advantage of available federal and state tax credits before they expire). Monetary incentives are the most compelling: 71 percent of customers adopt renewable energy sources to lower their utility bill, and 12 percent to take advantage of tax credits. Still, nearly a fifth (17%) claim they invested in renewable energy generation in response to environmental concerns.

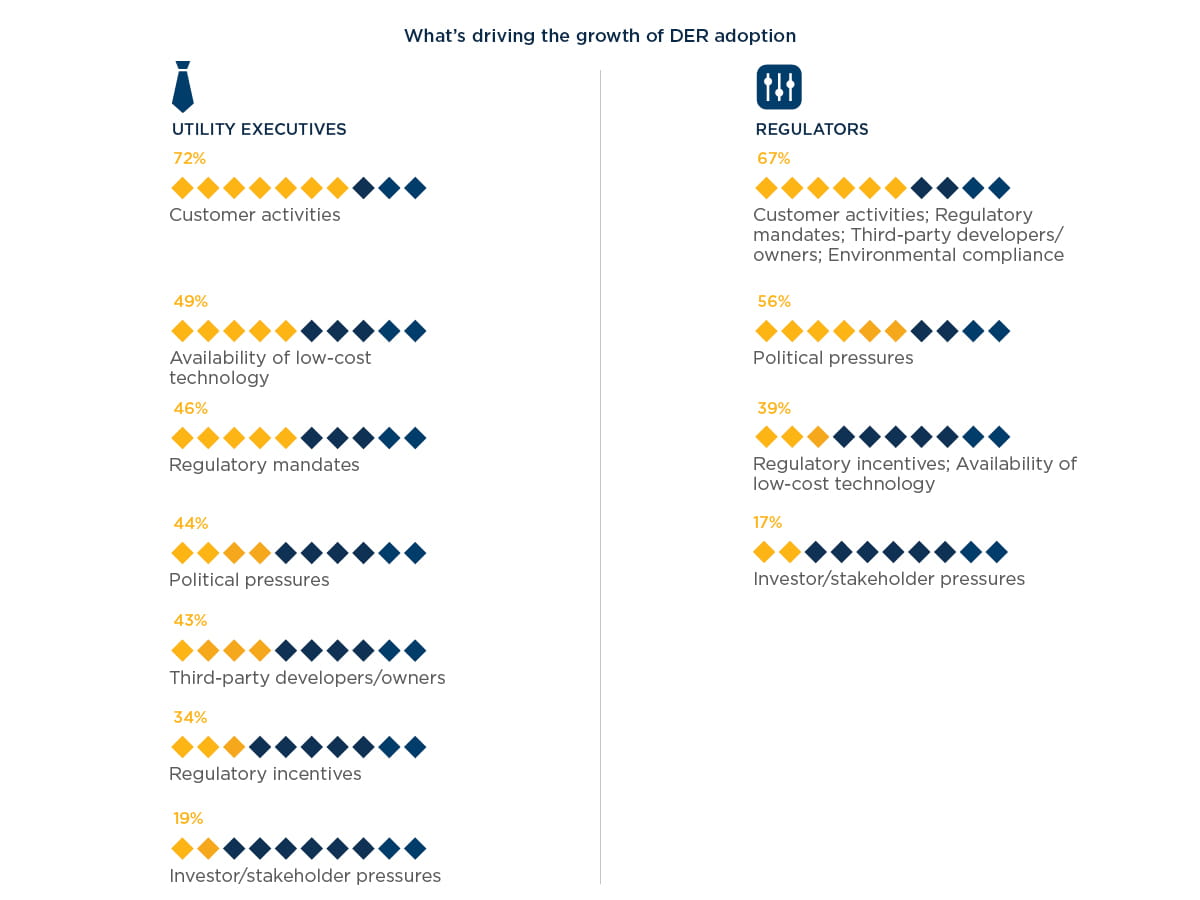

Utility executives and regulators also ranked the top factors encouraging the addition of DERs to their systems and jurisdictions. While both groups call out customers’ influence, their opinions on the power of politics, technology and third parties diverge.

Utility executives and regulators agree that customer interest and initiative is driving DER adoption; regulators tend to inflate their own influence over this trend, whereas utility leaders feel technology plays a larger role than regulatory or public policies. According to utility leaders, a handful of technical factors have also supported DER penetration on utility systems, including two-way meters, enhanced telecommunication systems and virtual net metering.

Chapter 3: Accounting for known unknowns: Planning for the future of DERs

The utility industry to date, has only seen a glimpse of how DERs stand to transform its business model, policy framework and customer relationships. Across stakeholders, there are varying predictions about when DERs will reach a critical tipping point.

Compared to utility executives, regulators are more likely to feel that DERs will be prevalent enough to necessitate significant operational and management changes in the near future. Seventy-five percent of regulators believe this tipping point will occur when DERs account for between one and 10 percent of system penetration. Almost half (49%) of utility leaders believe the tipping point range will fall between 11 and 25 percent of system penetration.

Utility executives across the country hold a conservative outlook toward the spread of distributed energy resources within their systems. The majority (68%) expects that DER technologies will provide one to five percent of supply resources in the next five years. Customer on-site generation will likely account for the bulk of this growth: 47 percent of executives believe small residential systems will be the most prevalent source of DERs on their systems in the next five years, followed by third-party power providers, the utility itself, and commercial/industrial systems.

Barriers to accommodating distributed energy resources

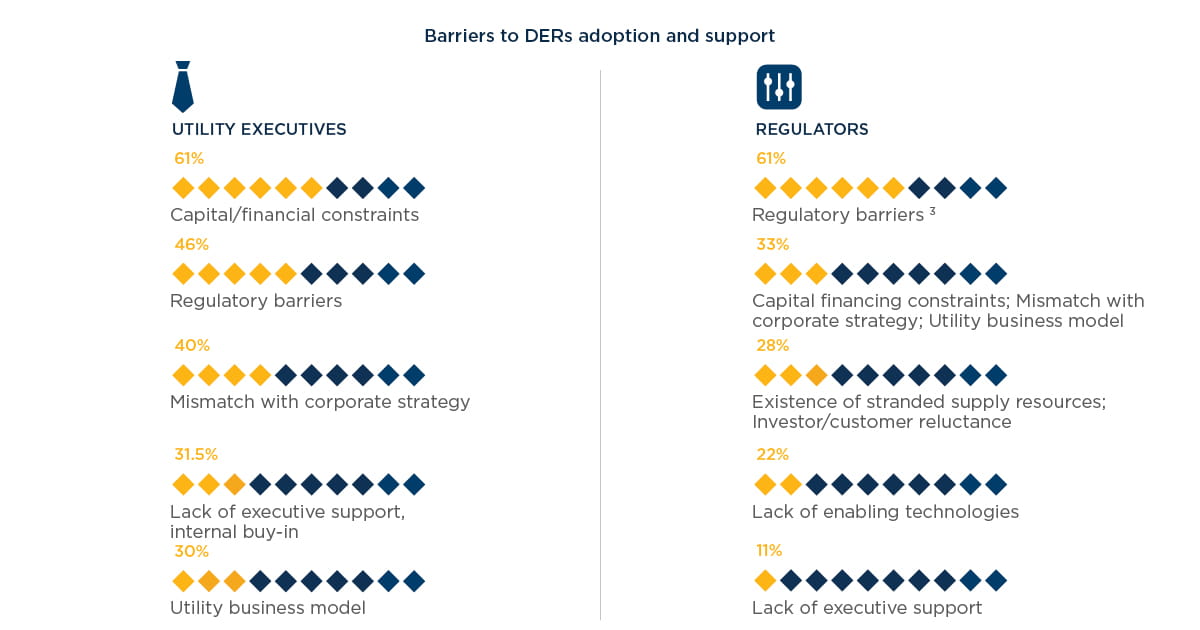

Supporting DERs and integrating them into daily utility operations will not come without challenges. Utility executives and regulators, however, have contrasting ideas about the obstacles to utility investment in DERs, DER support systems, and necessary services.

Regulators widely perceive their own activities as the primary hurdle to greater DER investment, but utility executives feel the main issue stems from financial constraints and other internal friction. Utility leaders are almost three times more likely than regulators to report lack of executive buy-in as an obstacle to DER support. The larger the gap between both groups’ perceptions, the more complicated it will be to smoothly encourage and increase DER adoption. Regulators hoping to promote utilities’ DER investment need to tailor their strategies to the issues executives face, addressing not only legal and regulatory requirements but also customer affordability and utility revenue cost recovery assurances.

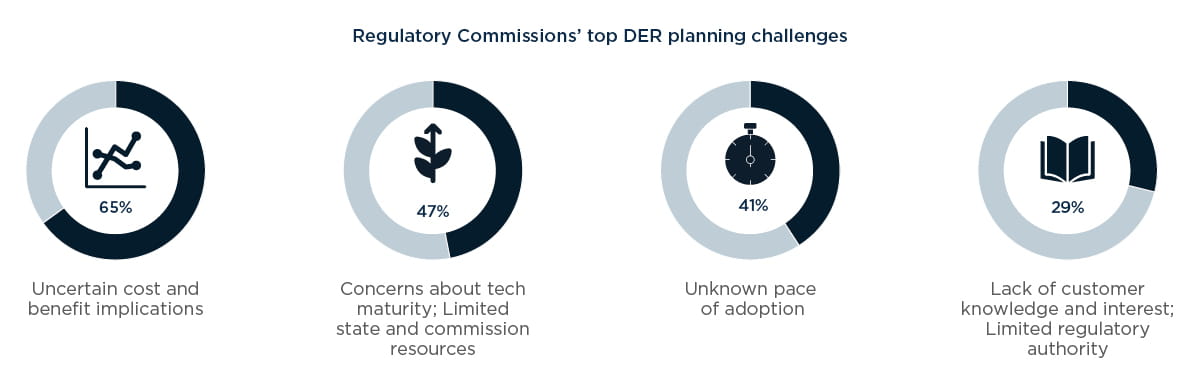

At the same time, DERs present a handful of planning hurdles for regulatory commissions to overcome. Given how new distributed resources are relative to other forms of utility infrastructure, regulators can only act on generalized and often anecdotal evidence about the technology’s long- term financial impact and future innovations.

Regulators’ responses hint that intervention (and support) may be needed at a higher level in order for commissions to authorize utility funding for research and pilot projects and provide the commissions the mandate to plan for the future of DERs and accommodate both utility and customer demands.

Utilities’ planned changes to account for DERs

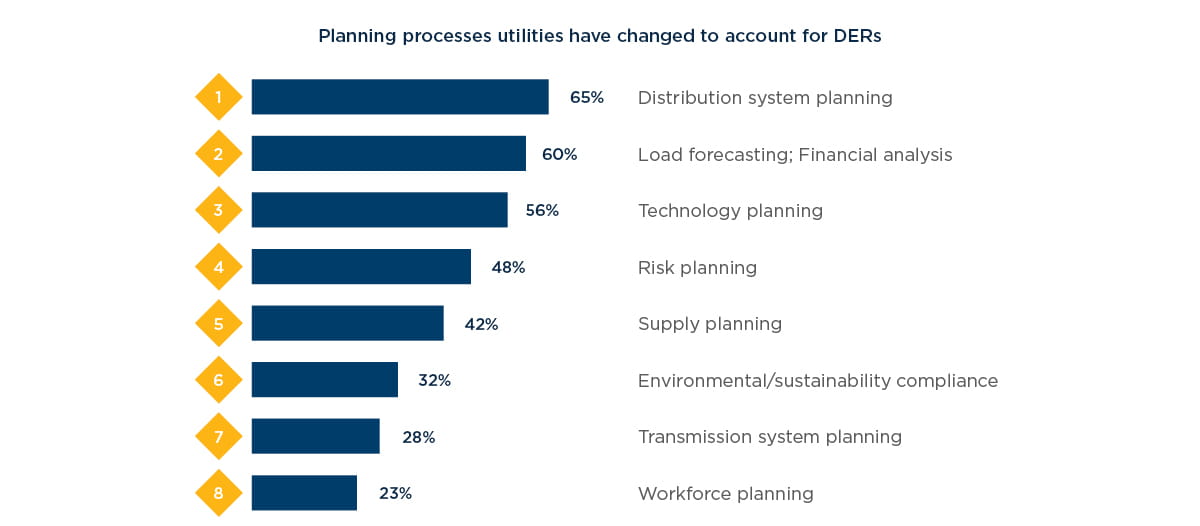

Fortunately, utilities aren’t taking a complete “wait and see” approach to distributed energy resources. Many utilities have started to tweak portions of their internal planning processes to compensate for the operational impact of DERs. Core operations including electricity distribution systems, forecasting, and technology integration are at the center of these initial changes, with issues such as environmental compliance and workforce planning on the periphery.

With the number of local regulatory commissions that have launched grid modernization initiatives – many of which require utilities to submit plans for meeting renewable energy goals – utilities may need to put greater emphasis on sustainability compliance. Similarly, utilities that treat workforce planning as an afterthought could run into challenges if their employees aren’t equipped to respond to and remedy DER customer issues and network challenges that can accompany larger scale penetration of DERs on their systems.

Even with most utility executives expecting DER penetration to be limited to five percent of load in the next few years, leaders are still considering a handful of large-scale internal initiatives to prepare for the growth of non-utility owned resources on their systems. Some regulatory agencies are lifting the cap on DERs and requiring utilities to deal with the potential onslaught of DER growth. Almost two-thirds (65%) of participating executives are looking at changing their utilities’ revenue models or modifying their internal planning methods (59%). Around half (52%) are contemplating expanding their utilities’ distribution planning to integrate customer resources, and a similar amount (47%) may edit their approach to planning for compliance with new and pending environmental regulations. Less than one-third (32%) of executives are considering offering new customer planning or DER management services.

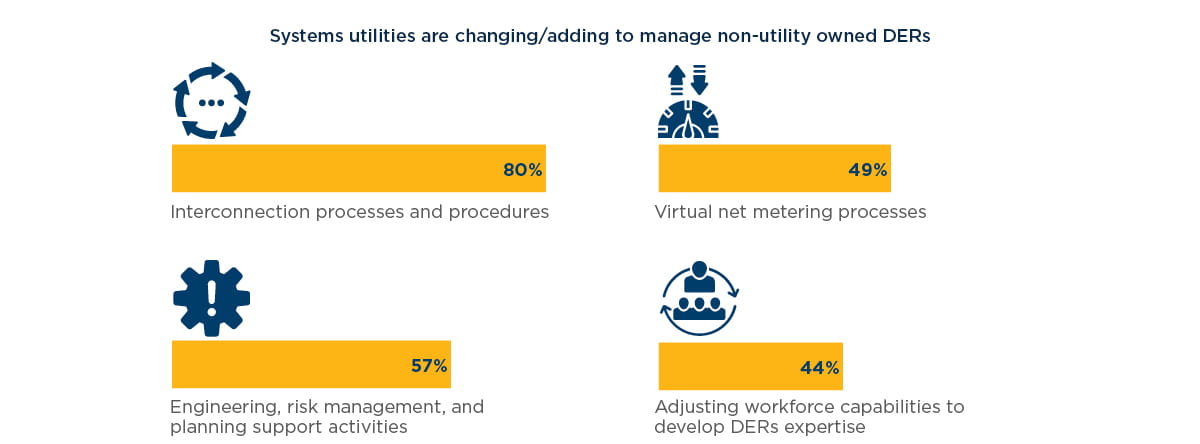

Beyond these broader processes, utility leaders are also enhancing (and adding) specific activities to support DERs integration and management:

Interconnection and virtual net metering processes are critical to facilitating customer integration with the utility grid, and thus represent a key point of engagement for DER adoption. Engineering and risk activities, on the other hand, are essential for utilities to accommodate generation and ancillary service requirements for customer-sited DERs. That few utilities plan to invest in DER support services could explain why less than half are adjusting their staff’s skillsets to include DERs expertise.

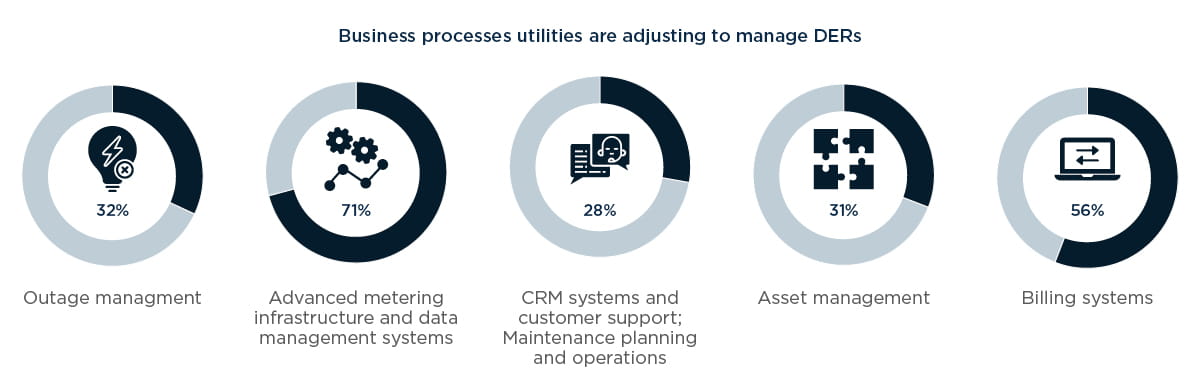

Utilities’ efforts to accommodate DERs will depend largely on having the right internal and customer-facing technology in place. Many organizations are beginning to reevaluate both. Once again, utility leaders place a greater emphasis on technologies directly tied to ongoing operations, generation and distribution rather than those that impact the customer experience.

Though utility executives consider DERs to be both an opportunity and a threat, many of utilities’ planned operational changes appear to be directed at protecting revenue, not supporting or satisfying customer demands around DER support. In practice, utility executives may perceive distributed energy resources to be more of a risk to their businesses than an opportunity. Until the policies crystallize, utilities are much more likely to take steps to minimize business threats rather than dive headfirst into DER support – and risk regulatory penalties in the process.

How regulators are evolving to support DERs

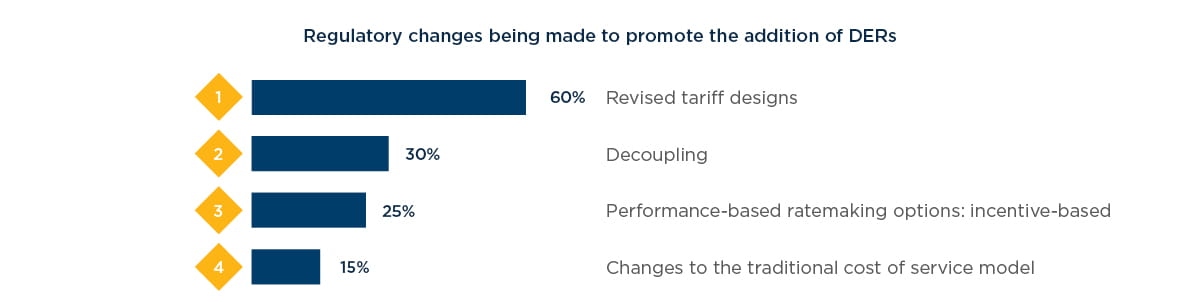

Distributed energy resource adoption requires action from both utilities and regulatory commissions. Utilities are trying to find their place in the market for DERs and regulators are rethinking their own processes and policymaking to encourage DER growth. As the following chart details, most regulators believe altering tariff designs is the most appropriate approach, while other more radical methods (such as decoupling and performance-based ratemaking) garner less support.

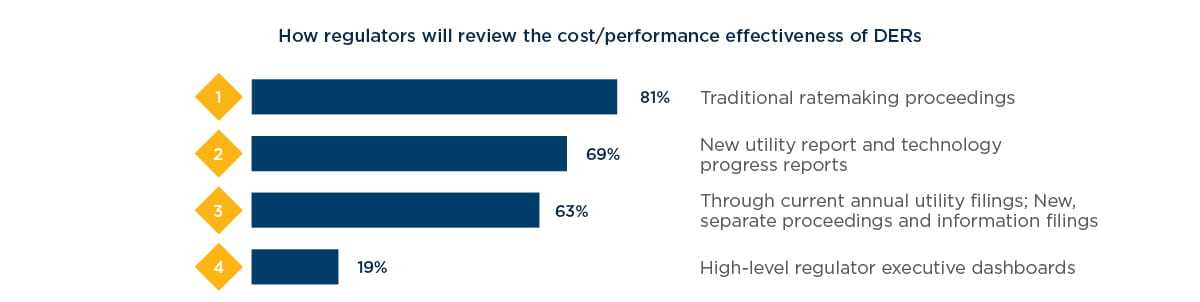

More than three-quarters of regulators (77%) also plan to formally review the technology cost and performance effectiveness of DERs, but some authorities may take more traditional approaches to doing so than others. Regulators are using “cost of service” standards to assess the cost effectiveness of DERs through traditional regulatory proceedings, when in fact, such costs are more market-driven and do not necessarily lend themselves to a cost-of-service benefit/cost assessment. Markets can set prices higher or lower than prices determined by regulators, thereby affecting the perceived cost-effectiveness of DERs. As a result, return on investment would be higher or lower for DERs depending on how prices are set.

In regards to assessing DERs’ financial effectiveness, regulators are keen on taking a non-invasive approach; the majority of commissions plan to rely on traditional proceedings and current utility filings for conducting these reviews. This may be less disruptive in the short term, but using dated methods to measure an emerging technology could skew the data and cause more confusion later on. The approach being used suggests a need for more current market-based tests for

cost effectiveness, tying in the personal and intrinsic value that extends beyond energy and environmental benefits. Risk transfer is important here, as returns on equity will vary depending on whether prices are market-based or cost-of-service based.

Conclusion

Greater adoption of distributed energy resources is more a question of “when” than “if.” Utilities and regulators agree that they must collaborate in order to address the challenges to DER investment, protect utility revenue streams, and support customers interest in DER. Residential customers’ DER adoption may not seem remarkable now in many parts of the U.S., but this audience is clearly positioned as a major driver of renewable energy’s future growth.

On a positive note, utilities and regulatory commissions are not sitting idly by waiting for DER adoption to grow; they’re considering and implementing changes to support and accommodate such resources. For example, the New York State Public Service Commission is rethinking the traditional role and purpose of regulated utilities in its recently announced “Reforming the Energy Vision” initiative, a strategy intended to promote clean energy innovation and improve the utility customer experience. The California Public Utility Commission has also proposed a slate of innovative plans to accommodate DERs as part of its Distribution Resource Plan proceeding. The Massachusetts Department of Public Utilities has required utilities to prepare a business case for proposed grid modernization plans encompassing a wide-range of technologies, including DERs.

Other commissions across the country are actively addressing issues such as net metering, increasing or lifting the cap on net-metered loads, looking to capture the value of solar credits, and considering support for community solar systems. All of these initiatives, while rebranded or called something different, are an extension of the “utility of the future” and “utility 2.0” work started a decade ago. As the industry’s DER knowledge base grows and technologies proven, businesses, customers, and regulators will continue to look for ways to unlock value from these markets. Likewise, the promulgation of final rules implementing the U.S. Environmental Protection Agency’s Clean Power Plan for reducing carbon emissions from power generation is requiring a fresh look at how DERs might support CPP carbon reductions.

Still, there’s more work to be done. Regulators need a better approach to understanding utilities’ challenges in order to create and adjust policies in ways that eliminate the barriers to DER support. This may start with more closely weighing the merits of utility versus non-utility DERs ownership. Specifically, regulators must focus less on rates and more on costs, and identify methods to help utilities address reliability and resiliency as generation occurs closer to load. They should also investigate new risk and revenue-sharing mechanisms to foster innovation, unlocking value from the utilities’ trove of real-time information and the potential of performance-based ratemaking.

Part of the burden to evolve falls on utilities as well. Utility leaders need to start treating DERs as an opportunity more than a threat, concerning themselves as much with customer satisfaction as with revenue protection. From the utility provider perspective, it is not enough to have DERs on the grid. Given intensifying concerns about grid reliability, utilities can pursue new revenue streams by integrating DERs more closely into their systems and honing their distribution services. Utilities have a chance to expand their business model and strengthen customer relationships by delivering continuous DER support, and simplifying the DER application, integration, and support process.

As utilities struggle to plan for and incorporate DERs into their existing resource plans, it is important to realize that a crop of alternative business models is emerging. There are several avenues for utility

leaders to explore, from investing in third-party projects to managing community solar projects in lieu of disaggregated rooftop solar assets. Another route gaining traction throughout the sector is to invest in DERs via unregulated subsidiaries, as AES did through its acquisition of Main Street Power, or Duke Energy through its investment in REC Solar.

The utility industry’s status quo has reached an inevitable turning point. If utilities and regulators make a concerted effort to confront these changes, everyone – including customers – can endure the growing pains and realize economic, social, and environmental benefits.

Methodology

West Monroe surveyed nearly 2,000 customers, 109 utility executives and managers in major markets across the country, and interviewed dozens of regulatory commission chairpersons, commissioners and senior staff. The goal of this research was to understand customer attitudes toward DER adoption, the broader impacts DERs will have on U.S. utility operations, and what both utilities and regulatory bodies are doing (or plan to do) to accommodate DERs from strategy, process, technology and system integration perspectives. Key findings from the study include:

- 82% of utility executives say residential customers are adding DERs to their systems, more so than commercial and industrial users or the utility itself.

- 80% of utilities report having DERs on their systems, but only 37% have services, systems or technologies in place to support them.

- 49% of utility leaders feel DERs will reach a significant tipping point impacting operations when they account for 11 to 25 percent of their system generation; 75% of regulators feel the tipping point threshold is 1 to 10 percent

- 48% of residential customers are considering installing DERs for their homes in the next two years.

- 59% of utility executives say their organizations plan to make no or minimal investments to support DERs on their systems, unless mandated to do so.